Engaging self-employed people or Suppliers who offer a service (not goods)

Engaging self employed people for work

Engaging self employed people for work

As you will be aware we are carefully managing our budgets so one of the measures we’re taking is an additional approval process for all resourcing requests. For all Professional Service roles this form will now go for approval to your Divisional Director and then to the Registrar before a TR8 is taken forward. For any questions please speak directly to your Divisional Director.This should be done prior to starting the IR35 process.

University Business Rules relating to Contract for Services and the Self Employed:

- This method of engagement must only be used where no other arrangement is appropriate.

- The engagement must be funded from within the College/Service budget or other agreed staffing budget.

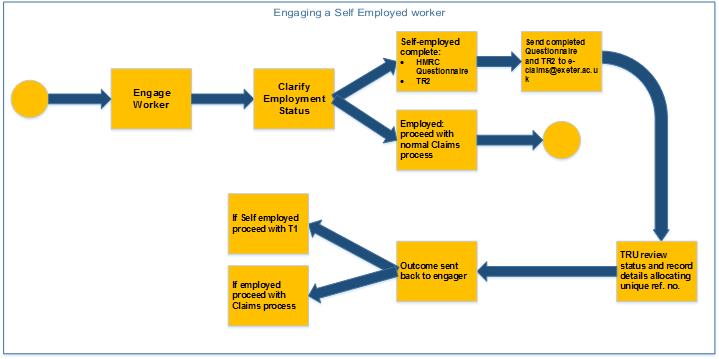

- The engager must follow IR35 Processand complete forms including HMRC Questionnaire prior to the work commencing.

- The IR35 Process is mandatory for all self employed engagements - in the UK and overseas.

IMPORTANT - Be aware: it is University Policy that current employees cannot undertake additional work for the University on a self-employed basis, even where the services will be paid through a limited company or other business structure. Any engagements considered 'exceptional circumstances' must be agreed in advance with the HR Partner and signed off by the University Tax Manager.

For any engagements considered ‘exceptional circumstances' where the work has already been completed payment will be made through payroll. In this instance any future work must be agreed in advance and escalated to the University Tax Manager.

See below for details about when to follow the IR35 Processand take required actions.

Most individuals engaged to conduct work for the University are employed via a contract of employment which is either:

- Permanent (open-ended)

- Temporary (fixed term)

- or Casual via our Temporary Resourcing Unit

There are occasions when the University may need to engage an individual or company for ‘services’. This could include work done on a very short-term or one-off basis (e.g. to deliver a lecture on a specific topic or contribute expertise to a particular project) or could involve a more long term project.

Where ‘services’ are procured on a self-employed, OR other business structure basis (this includes contractors through an agency) a ‘contract for services’ may be appropriate. In these circumstances the IR35 Process must be followed.

Self-employed workers are not entitled to statutory employment rights.

IR35 Tax Legislation states that where an individual offers services through a company (self-employed and Personal Services Companies) and the nature of the relationship is more akin to an employee, then the individual should be taxed and pay national insurance as if they were an employee. In this case we pay via our casual claims process. If the nature of the work is truly self-employed, then we can pay via our standard procurement process (e.g. invoice).

See below for more information

It is the responsibility of the College or Service engaging an individual to make the initial determination whether the engagement is self-employed (contract for services) or should be paid via our casual claims so that tax and NI can be deducted. This will then be checked by the IR35 Team.

In the majority of cases it would not be deemed acceptable for employee of the university to be carrying out any additional work on a self-employed basis.

As you will be aware we are carefully managing our budgets so one of the measures we’re taking is an additional approval process for all resourcing requests. For all Professional Service roles this form will now go for approval to your Divisional Director and then to the Registrar before a TR2 request is taken forward. For any questions please speak directly to your Divisional Director.

1. Check employment status before any work starts. Each engagement must be checked in its own right according to the working arrangements required. Submit a TR8 request and attach a completed online HMRC Questionnaire result. Please ensure you include the name of the worker/company on the HMRC questionnaire.The TR2 will automatically come through to the IR35 team ir35@exeter.ac.uk.

IMPORTANT if there is a significant change in the scope of the work commissioned, a further review of employment status should take place to avoid an engagement developing into an employment relationship, or enable the engagement to be revised and paid via the payroll.

2. The TR2 should be completed at least 2 weeks before the work starts. The IR35 Team will then check compliance and return back your forms with a reference number providing you with advice on the next steps.

Employment Status Quick Guide:

- Permanent: An open ended role on our establishment

- Fixed Term Contract: A role on our establishment for longer than 12 weeks

- Casual: A short term role up to 12 weeks

- Contract for Services: A one off / occasional work

We offer workshops and IR35 Q & A drop in sessions for staff who contract with/engage in contracts for services. The workshops will demonstrate the IR35 process and explain the importance of compliance with this legislation.

These sessions will be attended by the University Tax Manager or the IR35 Advisor, the E-Claims Team and Procurement members and are an ideal opportunity to raise your questions/concerns about your existing contracts to get advice on any of the risks and steps to mitigate any future challenge from HMRC.

HMRC regularly conduct audits and some Universities have faced heavy penalties for noncompliance. We recommend to share this with relevant staff, and to come along to the sessions to ensure correct procedures are being followed.

Speak to the experts in our IR35 Q & A drop in sessions:

Dates: 11am first Wednesday of the month.

Please email ir35@exeter.ac.uk to request an invite.

Workshops (via Teams) coming up:

6 February 2024 11am -12pm

16 April 2024 11am - 12pm

TBC September 2024 11am - 12pm

Please email ir35@exeter.ac.uk to request an invite.

For further information and to put your name on the waiting list for a future workshop please email ir35@exeter.ac.uk.

Further workshop dates will published here depending on demand.

IR35 process

All forms should be completed and approved two weeks before any work commences. This will allow for the engagement of temporary workers process to run smoothly.

IR35 taxation laws ensure that where an individual offers services through a company to a third party (such as the University) and the nature of the relationship is no different to being an employee of the University, then the individual should be taxed as if they were an employee.

PSC are usually:

- Limited Company or Partnership

- One majority shareholder (or with spouse, partner or dependant)

- Individual is main beneficiary from services provided

- Likely to be only employee

- Work is similar to that of an employee

The key issues to consider are:

- Would the positon normally be filled by an employee?

- Can the Personal Services Company supply a substitute and pay the substitute and in reality is this practical based on the nature of the work being carried out?

- Can the University move the “contractor” to a different task or project than they originally agreed to do without issuing a new contract or re-negotiating the current contract?

- Who decides how the work is to be carried out – the University or the “contractor”? (“Control”) This includes whether the “contractor” is required to follow University’s procedures and receive instruction which apply to employees; who decides the schedule of working hours; where the “contractor” carries out their work. This less autonomy the “contractor” has, the more likely the relationship is to be akin to employment.

- What does the “contractor” have to provide for the engagement? If the University provides an office, laptop, telephone, email address etc.. then the relationship is more likely to be akin to employment.

- How is the “contractor” paid for the engagement? An hourly, daily or weekly rate is more likely to be akin to employment whereas a fixed price for a specific piece of work, payable on completion will point towards a genuine contract for services.

- If the University is not satisfied with the “contractors’” output, would the “ contractor” have to put it right in their usual working hours at the usual rate of pay (more akin to employment) or in their own time and at their own expenses (more akin to contract for services).

University Staff who engage a personal services company to carry out work must assess their employment status. If the result shows they are bound by the IR35 rules, the worker should be engaged through HR. If not, they should be engaged through the Procurement route.

Further information can be found by downloading: Payment options for one-off or short term assignments

Procurement and best value

Good procurement provides the right outcome, best whole-life cost, legal compliance, reduces risk and introduces innovation. Advice is readily available on the Finance pages online.

The University is committed to implementing policies and procedures that support sound procurement practice and that act in a non-discriminative manner when dealing with both existing and potential suppliers. The aim is to promote engagement to encourage best provision and innovation thus improving the University’s reputation and professionalism. Integral to the competitive process is that suppliers should be treated fairly and openly and be given equal opportunity to bid for work if they can meet the needs and requirements of the University.

Colleges and Services should ensure a competitive/tender process takes place when procuring any goods and services clearly stating the relevant and appropriate requirements for those goods and services in terms of best quality and price. Such planning is vital and will enable beneficial and competitive outcomes.

For further information please refer to the Procurement buying page.

Professional service roles approval form (please note this should be completed before the TR8)

HMRC Questionnaire For ease of processing please add details i.e. name, date and role of service provider, to the outcome pdf.

Contract for Services: Terms and Conditions

PPE Template (Permitted Paid Enagagement visitor)